The steady collapse of Nike is vastly underreported and follows the classic rise-and-fall pattern of corporates (with one new twist at the end).

Initially, someone comes up with a really good product and a business is born. As the product is sold in more places to more people, volumes drive operating leverage, and the business grows into a global group, with the brand becoming a household name.

Read:

Nike lays off 775 workers as it boosts use of automation

Adidas lifts profit target as Samba boom withstands tariffs

And then, through a steady succession of professional CEOs – more and more removed from the actual product – the group realises that the brand is strong enough to raise prices well in excess of inflation without materially denting volumes (maybe they even grow), and from this point, prices drive revenues more than volumes, and operating leverage creates profit growth.

Listen/read:

Can Nike get its mojo back?

Nike Dunk, once the world’s hottest sneaker, is fading away

Eventually, however, price increases hit a consumer affordability wall (typically at a point when the quality of the product has been steadily cut to bolster margins). Suddenly price hikes stall and slipping volumes accelerate downwards, with operating leverage viciously decimating the bottom line.

And everyone is very surprised, especially the professional CEO at the time.

Add to this story the fact that Nike largely pioneered the direct-to-consumer(DTC) business model – which aimed to sidestep wholesalers and retailers in order to bolster its own margins and own the consumer’s loyalty.

At first, this was a marvel and really worked, but then Nike got greedy and decided to cut ties with major wholesalers to force consumers into its own higher-margin DTC channel.

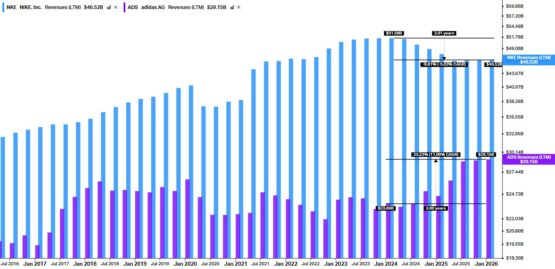

It did not work (see graph below).

Wholesalers found other shoe companies to supply them, retailers had empty shelf space they promptly filled with new shoes, and consumers were suddenly exposed to new, cheap, and arguably better quality branded shoes!

ADVERTISEMENT

CONTINUE READING BELOW

Overnight – initially perhaps hidden by a Covid rebound, but very clear in the post-Covid era – Nike lost the consumer, and it shows.

Revenue – Nike vs Adidas

Source: Koyfin

Over the past two years, Nike’s sales have declined at a 5% year-on-year compound annual ‘growth’ rate (CAGR), while rival Adidas’s have grown at 11%.

And what is going to change?

Consumers have now found better, cheaper shoe brands and fostered new loyalties, while wholesalers and retailers have been burned and are in no rush to give Nike the benefit of the doubt.

Once you’ve lost the consumer at the retailer, you also lose them to your DTC channel.

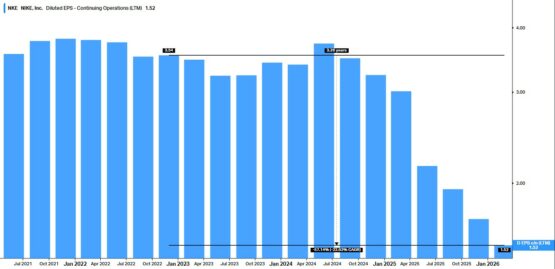

And let’s be honest, the decades of success at Nike bred a bloated cost structure that is always painful to rightsize, thus the negative operating leverage cuts deeply into its collapsing profits (more than halving over the above noted period and dropping by 23% year-on-year – see chart below).

Nike’s diluted earnings per share (EPS) from continuing operations

ADVERTISEMENT:

CONTINUE READING BELOW

Source: Koyfin

Isn’t this article about Levi Strauss & Co?

Years ago, I identified Levi Strauss and its DTC strategy as the potential ‘next Nike’ (Is Levi Strauss the next Nike?) – and given Levi’s stunning results last week, I thought it was perhaps time to revisit that view – and hope that I was perhaps wrong.

The short answer is that we had not yet seen how DTC could collapse, as Nike’s slow-motion mistakes had not yet been revealed by its aggressive cutting out of wholesalers and retailers. We were still under the delusion that Nike was a well-run business.

But we are now wiser, and thus, in a two-part series, I thought I would first unpack Nike’s collapse before going on to look at how Levi Strauss is doing.

Check back here in a fortnight for Part II …

* Keith McLachlan is CEO of Element Investment Managers.

* Portfolios managed by McLachlan may hold Levi Strauss shares.

#Levis #Nike